Second- and third-order Greeks — vanna, charm, vomma, speed — that describe how delta, gamma, theta, and vega themselves change with market conditions. Negligible on single-leg trades at 0.20 delta but critical for large portfolios and dealer hedging.

⚡ KEY TAKEAWAY: For single-leg sellers at 0.15–0.30 delta, higher-order Greeks are noise. For portfolio-level risk or multi-leg structures, they explain the moves first-order Greeks miss.

Why It Matters

First-order Greeks tell you your current exposure. Higher-order Greeks tell you how that exposure will change. For single-leg OTM sellers at 0.20 delta, they're noise. For multi-leg books or large portfolios, they explain why P&L diverges from what delta and theta predicted.

How It Works

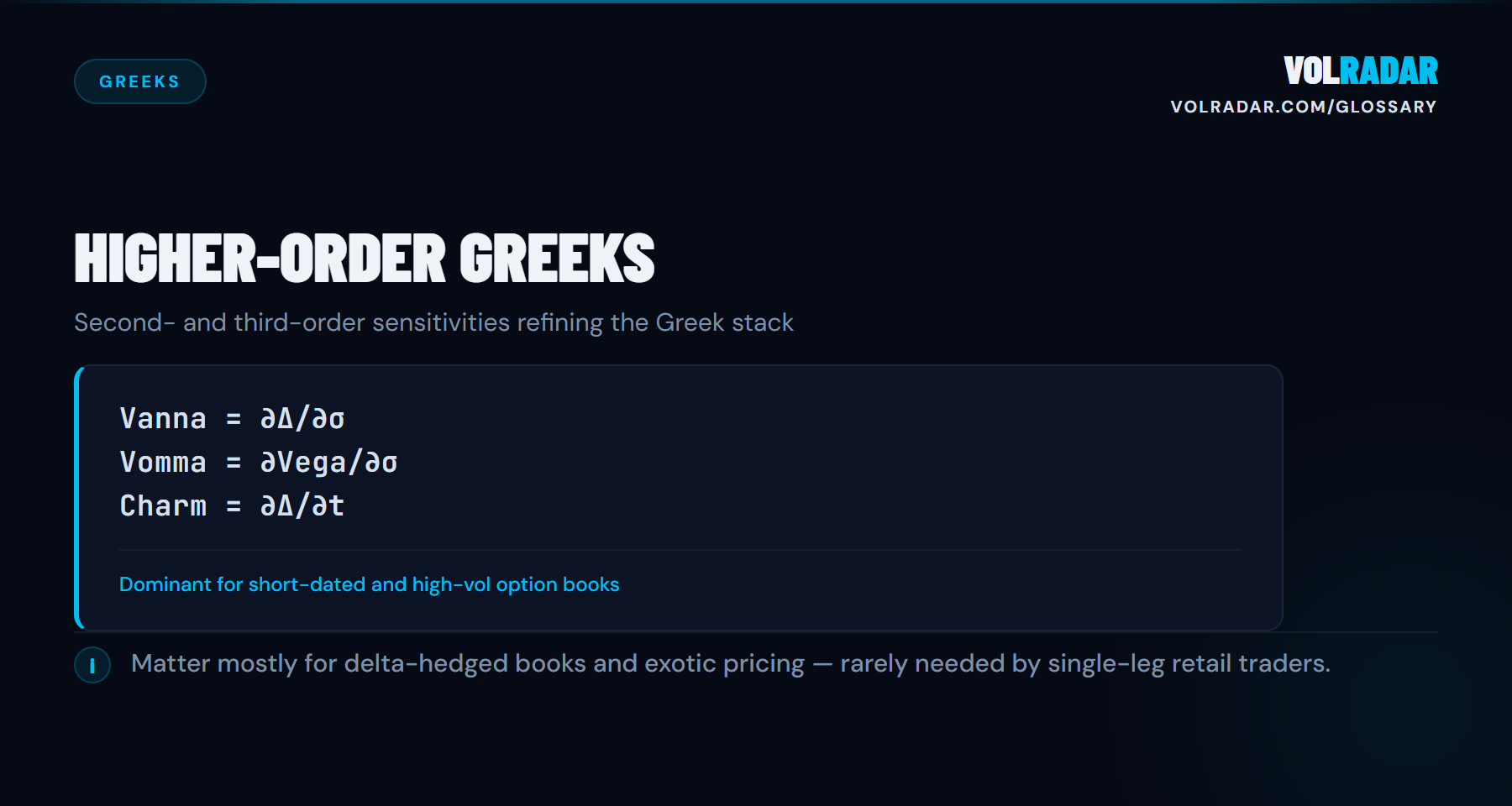

Higher-order Greeks are partial derivatives of the primary Greeks. Vanna = ∂Δ/∂σ (delta's sensitivity to IV). Charm = ∂Δ/∂t (delta decay). Vomma = ∂vega/∂σ (vega's convexity). Speed = ∂Γ/∂S (gamma's acceleration). Each captures a dimension of risk that first-order Greeks hold constant.

Example

You sell a 0.20 delta put on SPY. Delta says you're short roughly 20 shares of exposure. But if IV spikes 5 points, vanna pushes your delta to 0.28 — now you're effectively short 28 shares. The extra 8-share exposure came from a Greek you never tracked.

Common Mistakes

Trying to manage higher-order Greeks on small retail positions — the transaction costs outweigh the risk reduction. Also: treating vanna and charm as exotic concepts when they directly explain why your delta drifted overnight without any price move.

Second- and third-order Greeks — vanna, charm, vomma, speed — that describe how delta, gamma, theta, and vega themselves change with market conditions. Negligible on single-leg trades at 0.20 delta but critical for large portfolios and dealer hedging.

Why does Higher-Order Greeks matter for premium sellers?

For single-leg sellers at 0.15–0.30 delta, higher-order Greeks are noise. For portfolio-level risk or multi-leg structures, they explain the moves first-order Greeks miss.

How does Higher-Order Greeks work?

Higher-order Greeks are partial derivatives of the primary Greeks. Vanna = ∂Δ/∂σ (delta's sensitivity to IV). Charm = ∂Δ/∂t (delta decay). Vomma = ∂vega/∂σ (vega's convexity). Speed = ∂Γ/∂S (gamma's acceleration). Each captures a dimension of risk that first-order Greeks hold constant.

What are common mistakes with Higher-Order Greeks?

Trying to manage higher-order Greeks on small retail positions — the transaction costs outweigh the risk reduction. Also: treating vanna and charm as exotic concepts when they directly explain why your delta drifted overnight without any price move.