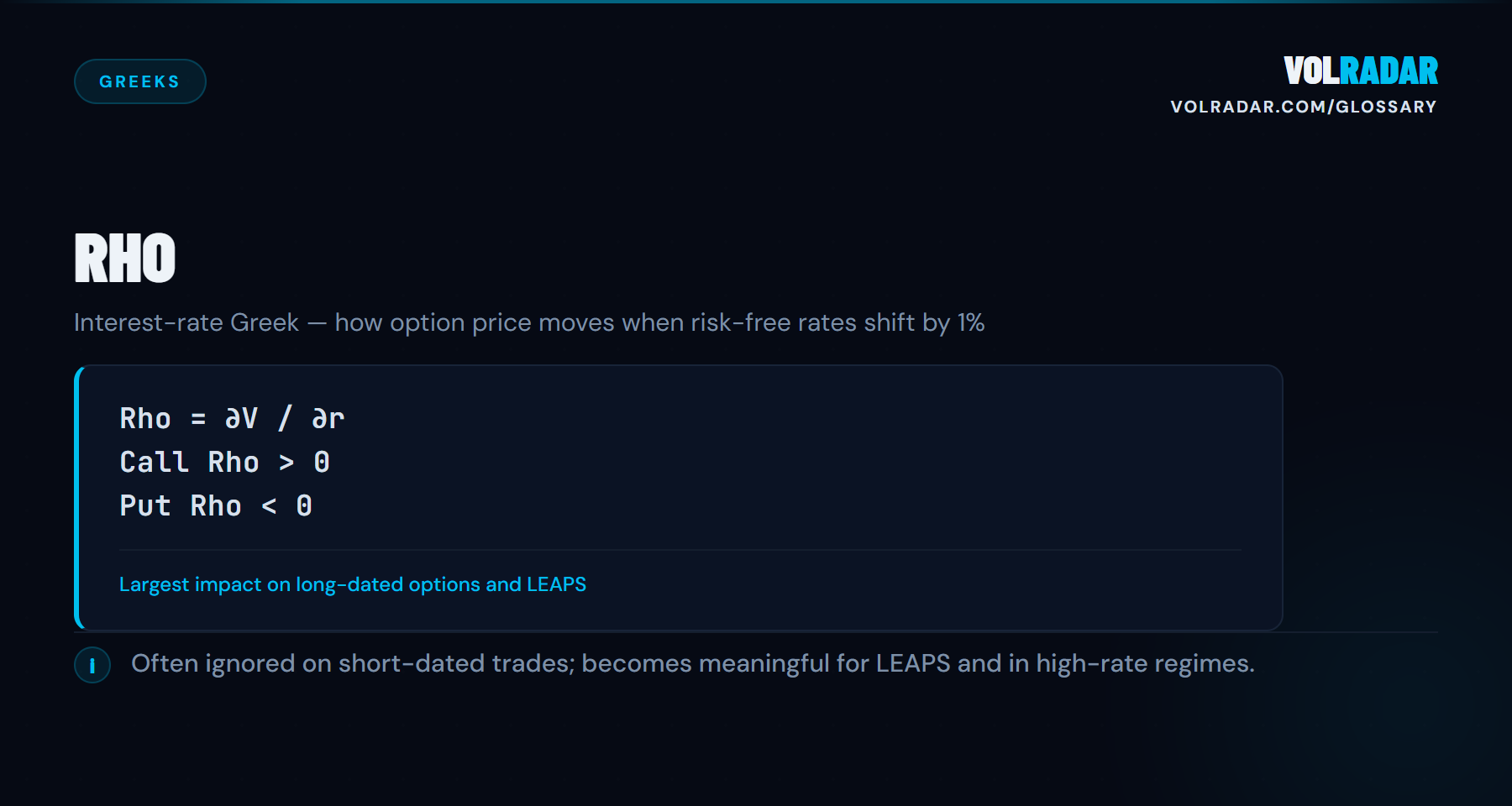

The rate of change in an option's price for a one-percentage-point move in the risk-free interest rate. Rho is the smallest of the five main Greeks for short-dated options, but it can dominate P&L on LEAPS and long-dated diagonals when the Fed moves.

⚡ KEY TAKEAWAY: Ignore rho on anything under 90 DTE. For LEAPS and diagonals, a 50 bp rate surprise can move the position more than a day of theta.

Why It Matters

Rho is irrelevant for most short-dated trades. But if you hold LEAPS, diagonals, or any position with 6+ months to expiration, a single Fed decision can move your P&L more than a full day of theta. Ignoring rho on long-dated positions is like ignoring dividend risk on short calls — fine until it isn't.

How It Works

Rho measures how much an option's theoretical price changes per 1 percentage point move in the risk-free rate. Calls have positive rho (higher rates increase value); puts have negative rho. The effect scales with time to expiration — a 30 DTE option might have rho of 0.02, while a 500 DTE LEAPS can exceed 1.0.

Example

You own a 500-day AAPL $180 call with rho = 0.85. The Fed cuts rates by 50 basis points. Rho impact: 0.85 × (−0.50) = −$42.50 per contract, before delta, theta, or vega effects. On a $12 option, that's a 3.5% hit from rates alone.

Common Mistakes

Treating rho as always negligible. On 30–60 DTE trades it is, but on LEAPS it can dominate single-day P&L. Also: confusing the rho impact with the broader rate environment effect on stock prices — rho is the direct option-pricing sensitivity, not the equity market reaction.

The rate of change in an option's price for a one-percentage-point move in the risk-free interest rate. Rho is the smallest of the five main Greeks for short-dated options, but it can dominate P&L on LEAPS and long-dated diagonals when the Fed moves.

Why does Rho matter for premium sellers?

Ignore rho on anything under 90 DTE. For LEAPS and diagonals, a 50 bp rate surprise can move the position more than a day of theta.

How does Rho work?

Rho measures how much an option's theoretical price changes per 1 percentage point move in the risk-free rate. Calls have positive rho (higher rates increase value); puts have negative rho. The effect scales with time to expiration — a 30 DTE option might have rho of 0.02, while a 500 DTE LEAPS can exceed 1.0.

What are common mistakes with Rho?

Treating rho as always negligible. On 30–60 DTE trades it is, but on LEAPS it can dominate single-day P&L. Also: confusing the rho impact with the broader rate environment effect on stock prices — rho is the direct option-pricing sensitivity, not the equity market reaction.