Loading...

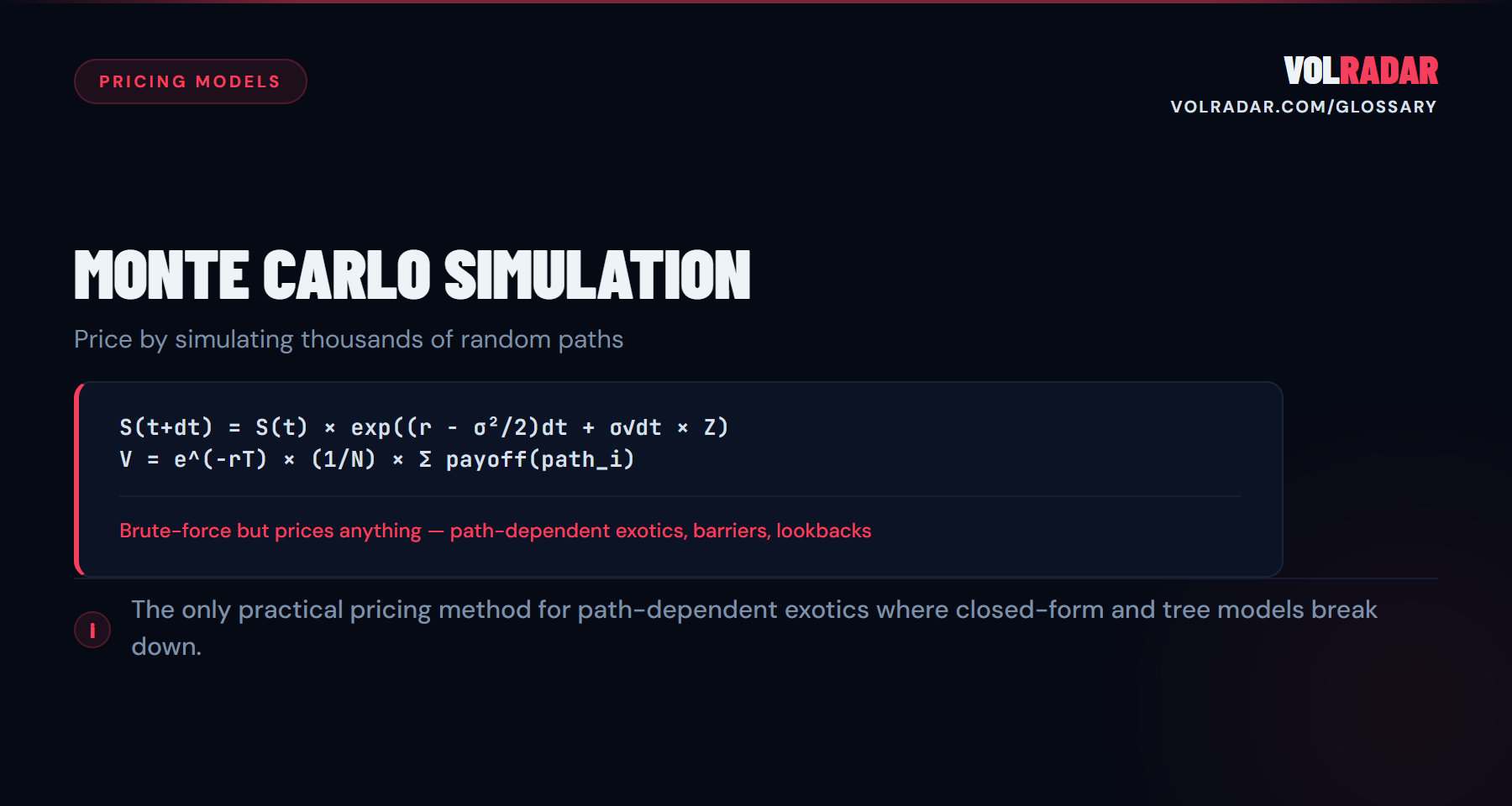

A numerical pricing method that generates thousands of random price paths for the underlying, calculates the option payoff on each path, and averages the discounted results. Brute-force but flexible — prices any payoff structure including path-dependent exotics.

⚡

Key takeawayMonte Carlo prices anything — barriers, lookbacks, Asians, multi-asset baskets. The tradeoff is speed: thousands of paths take compute time that closed-form models don't need.

💡 Why It Matters

Monte Carlo prices anything — barriers, lookbacks, Asians, multi-asset baskets, path-dependent exotics. When closed-form models can't handle the complexity, Monte Carlo brute-forces the answer by simulating thousands of possible futures.

⚙ How It Works

Generate N random price paths using geometric Brownian motion (or a more complex process). For each path, calculate the option payoff. Average all discounted payoffs to get the option price. More paths = more accuracy, but slower computation. Variance reduction techniques (antithetic variates, control variates) improve efficiency.

📋 Example

Price a down-and-out barrier call (knock-out at $90, strike $100, stock at $105). No closed-form solution exists. Run 100,000 simulated paths. 23,000 paths hit the $90 barrier and knock out (payoff = 0). The remaining 77,000 paths produce an average discounted payoff of $5.20. Option price ≈ $5.20.

⚠ Common Mistakes

Using too few paths and trusting the result. 1,000 paths gives a rough estimate with wide confidence intervals. 100,000+ paths are needed for reliable pricing. Also: Monte Carlo for plain vanilla European options is wasteful — Black-Scholes gives the exact answer instantly.

⚡ Monte Carlo Simulation in VolRadar

❓ FAQ

What is Monte Carlo Simulation?

A numerical pricing method that generates thousands of random price paths for the underlying, calculates the option payoff on each path, and averages the discounted results. Brute-force but flexible — prices any payoff structure including path-dependent exotics.

Why does Monte Carlo Simulation matter for premium sellers?

Monte Carlo prices anything — barriers, lookbacks, Asians, multi-asset baskets. The tradeoff is speed: thousands of paths take compute time that closed-form models don't need.

How does Monte Carlo Simulation work?

Generate N random price paths using geometric Brownian motion (or a more complex process). For each path, calculate the option payoff. Average all discounted payoffs to get the option price. More paths = more accuracy, but slower computation. Variance reduction techniques (antithetic variates, control variates) improve efficiency.

What are common mistakes with Monte Carlo Simulation?

Using too few paths and trusting the result. 1,000 paths gives a rough estimate with wide confidence intervals. 100,000+ paths are needed for reliable pricing. Also: Monte Carlo for plain vanilla European options is wasteful — Black-Scholes gives the exact answer instantly.

Related Terms

Bachelier Model

The Bachelier model (normal model) assumes the underlying follows an arithmetic Brownian motion with normally distributed returns, rather than the lognormal ...

Barone-Adesi-Whaley Model

The Barone-Adesi-Whaley (BAW) model is a quadratic approximation for pricing American options that decomposes the American option price into its European val...

Binomial Option Pricing

A discrete-time pricing model that builds a recombining tree of possible price paths.

Bjerksund-Stensland Model

The Bjerksund-Stensland model provides a closed-form approximation for pricing American options by treating early exercise as a flat barrier problem.

This is not financial advice. Read our full investment disclaimer.