Loading...

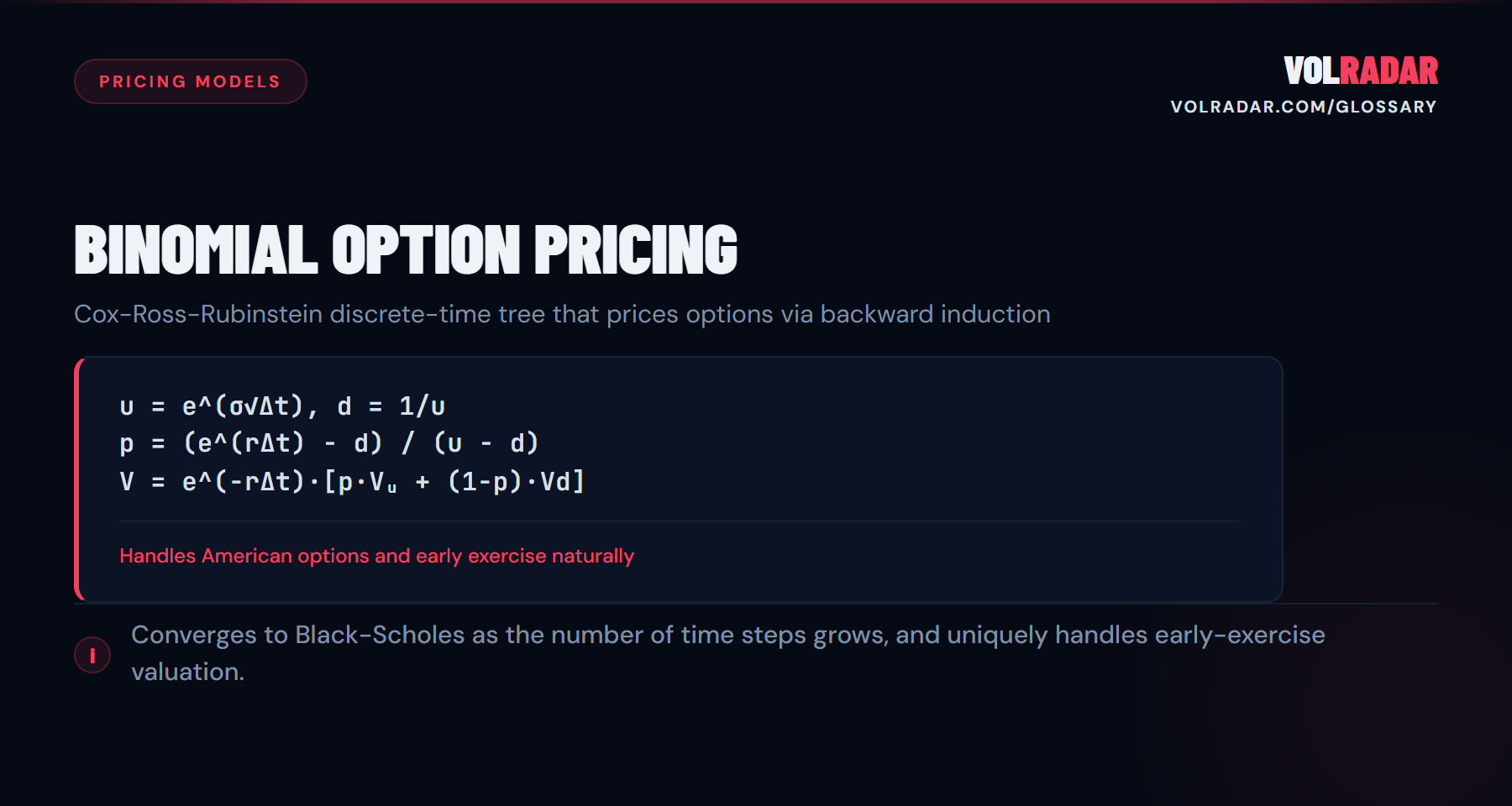

A discrete-time pricing model that builds a recombining tree of possible price paths. Unlike Black-Scholes, the binomial model handles American-style early exercise natively. Cox-Ross-Rubinstein (CRR) is the standard parameterization.

⚡

Key takeawayThis is how your broker actually prices American options. Black-Scholes gives the European value; the binomial tree adds the early-exercise premium on top.

💡 Why It Matters

The binomial model is how your broker actually prices American-style options. Black-Scholes handles European; binomial adds the early exercise decision at every node. If you trade US equity options, the price you see incorporates a binomial tree (or its numerical equivalent).

⚙ How It Works

Build a tree of possible price paths: at each step, the stock moves up by factor u or down by factor d. At expiration, calculate the option payoff at each terminal node. Work backwards through the tree, comparing the hold value (discounted expected payoff) to the exercise value (intrinsic) at each node. The greater of the two is the node's value.

📋 Example

AAPL at $200, $195 put, 30 DTE, σ = 25%. A 100-step CRR tree prices the put at $3.82. Black-Scholes (European) gives $3.75. The $0.07 difference is the early exercise premium — the value of being able to exercise on any of those 100 nodes if the stock drops far enough.

⚠ Common Mistakes

Thinking more tree steps always means more accuracy. Beyond 100-200 steps, the improvement is negligible. Also: binomial trees can be slow for exotic options with multiple path-dependent features — Monte Carlo is often better for those.

❓ FAQ

What is Binomial Option Pricing?

A discrete-time pricing model that builds a recombining tree of possible price paths. Unlike Black-Scholes, the binomial model handles American-style early exercise natively. Cox-Ross-Rubinstein (CRR) is the standard parameterization.

Why does Binomial Option Pricing matter for premium sellers?

This is how your broker actually prices American options. Black-Scholes gives the European value; the binomial tree adds the early-exercise premium on top.

How does Binomial Option Pricing work?

Build a tree of possible price paths: at each step, the stock moves up by factor u or down by factor d. At expiration, calculate the option payoff at each terminal node. Work backwards through the tree, comparing the hold value (discounted expected payoff) to the exercise value (intrinsic) at each node. The greater of the two is the node's value.

What are common mistakes with Binomial Option Pricing?

Thinking more tree steps always means more accuracy. Beyond 100-200 steps, the improvement is negligible. Also: binomial trees can be slow for exotic options with multiple path-dependent features — Monte Carlo is often better for those.

Related Terms

Bachelier Model

The Bachelier model (normal model) assumes the underlying follows an arithmetic Brownian motion with normally distributed returns, rather than the lognormal ...

Barone-Adesi-Whaley Model

The Barone-Adesi-Whaley (BAW) model is a quadratic approximation for pricing American options that decomposes the American option price into its European val...

Bjerksund-Stensland Model

The Bjerksund-Stensland model provides a closed-form approximation for pricing American options by treating early exercise as a flat barrier problem.

Black-76 Model

The Black-76 model adapts Black-Scholes for pricing options on futures contracts by replacing the spot price with the futures price and removing the cost-of-...

This is not financial advice. Read our full investment disclaimer.