Loading...

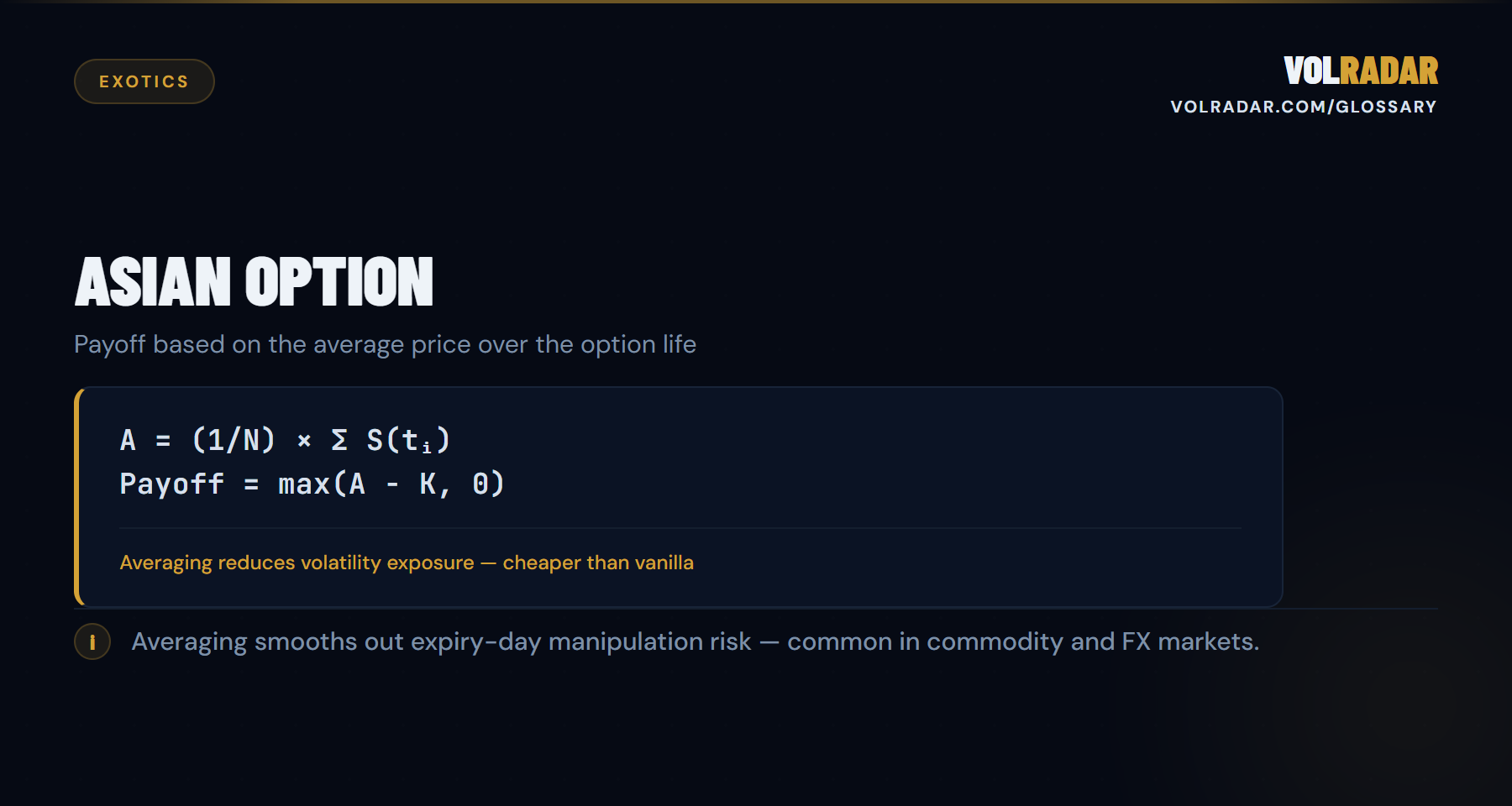

An exotic option whose payoff depends on the average price of the underlying over a specified period, not just the price at expiration. Averaging reduces the impact of outlier moves, making Asians cheaper than equivalent vanilla options.

⚡

Key takeawayAveraging kills tail risk — that's why Asians are cheaper. Common in commodity and FX markets where end-users want to hedge average costs, not spot prices.

💡 Why It Matters

Asian options use the average price over a period rather than the spot price at expiration. Averaging smooths out outliers, reducing volatility exposure and making them cheaper than vanilla. Common in commodity hedging where companies care about average cost, not spot.

⚙ How It Works

The payoff is based on the arithmetic (or geometric) average of the underlying price over predetermined observation dates. Call payoff: max(Average − Strike, 0). Because averaging reduces variance, Asian options have lower implied vol than vanilla options at the same strike.

📋 Example

A 90-day Asian call on crude oil, strike $75. The price is observed weekly (13 observations). At expiration, the average price was $78. Payoff: $78 − $75 = $3. Even though oil hit $85 at one point, the average smoothed the peak. An equivalent vanilla call at $75 would have paid $10 (using the final price of $85).

⚠ Common Mistakes

Comparing Asian option prices to vanilla option prices without adjusting for the averaging effect. Asians are always cheaper because the averaged payoff has lower variance. The discount is not a market inefficiency — it's the mathematical consequence of averaging.

❓ FAQ

What is Asian Option?

An exotic option whose payoff depends on the average price of the underlying over a specified period, not just the price at expiration. Averaging reduces the impact of outlier moves, making Asians cheaper than equivalent vanilla options.

Why does Asian Option matter for premium sellers?

Averaging kills tail risk — that's why Asians are cheaper. Common in commodity and FX markets where end-users want to hedge average costs, not spot prices.

How does Asian Option work?

The payoff is based on the arithmetic (or geometric) average of the underlying price over predetermined observation dates. Call payoff: max(Average − Strike, 0). Because averaging reduces variance, Asian options have lower implied vol than vanilla options at the same strike.

What are common mistakes with Asian Option?

Comparing Asian option prices to vanilla option prices without adjusting for the averaging effect. Asians are always cheaper because the averaged payoff has lower variance. The discount is not a market inefficiency — it's the mathematical consequence of averaging.

Related Terms

Barrier Option

An exotic option that activates (knock-in) or deactivates (knock-out) when the underlying price hits a preset barrier level.

Basket Option

A basket option has a payoff determined by the weighted average price of multiple underlying assets rather than a single asset.

Bermuda Option

A Bermuda option can be exercised only on specific dates between the purchase date and expiration, not continuously like an American option or only at expira...

Binary Option

An option with a fixed all-or-nothing payout: if the underlying finishes past the strike at expiration, the holder receives a fixed amount (typically $100); ...

This is not financial advice. Read our full investment disclaimer.