Loading...

Mechanics

Deep In-the-Money — Options Trading Term Explained

Deep In-the-Money Explained — definition, how it is measured, and why it matters for options research decisions.

By Aigars VolRadar·

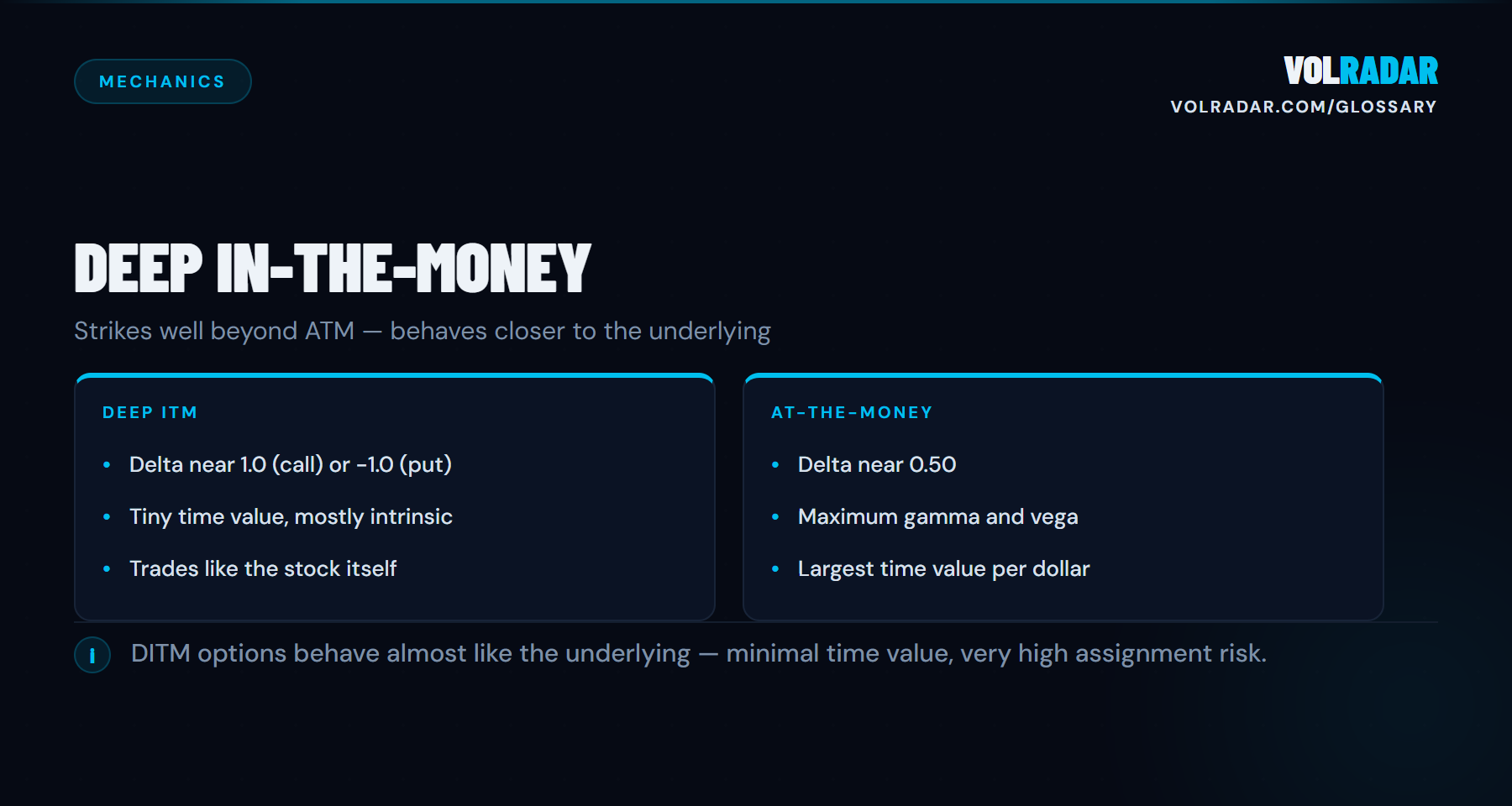

An option with a strike price significantly beyond the current underlying price, carrying high intrinsic value and minimal extrinsic value. Deep ITM options have delta near 1.0 and behave almost like the underlying stock.

Key takeaway

Deep-ITM options are stock substitutes, not volatility plays. Consider whether shares would be simpler.

Visual ReferenceVisual reference for Deep In-the-MoneyShowHide

Why It Matters

Deep ITM options behave more like stock than typical options, creating both opportunities and traps. With deltas above 0.85, these contracts track the stock nearly dollar-for-dollar while requiring less capital. Long-term investors use deep ITM LEAPS as stock replacement. For premium sellers, deep ITM short options carry high assignment risk, particularly around ex-dividend dates. Understanding this prevents unwanted assignments that can blow through margin limits overnight.

How It Works

Options with delta above 0.80 (calls) or below -0.80 (puts) are generally considered deep ITM. Intrinsic value dominates the premium and extrinsic value shrinks to a thin sliver. Gamma is low because delta barely changes with small price moves. Theta is minimal since there's little time value left to decay. The option essentially tracks the stock. Deep ITM calls often trade at parity near ex-dividend dates, meaning premium equals intrinsic value with no time value left. This signals the highest probability of early assignment — a critical watch point for covered call writers.

Example

MSFT trades at $420. The $370 call (50 points ITM) is priced at $52.80. Intrinsic value is $50.00, leaving just $2.80 in extrinsic. Delta sits at 0.94. If MSFT rises $10, this call gains roughly $9.40. The call costs $5,280 versus $42,000 for shares — a 7.9x capital reduction.

Common Mistakes

Selling deep ITM covered calls looks appealing but the premium is mostly intrinsic value you already own through the stock. Buying deep ITM options and ignoring the extrinsic value loss catches traders off guard. Holding deep ITM long options through ex-dividend dates when early exercise would capture the dividend more efficiently. Holding deep ITM long options through ex-dividend dates without evaluating early exercise is a missed opportunity. If remaining extrinsic value is less than the upcoming dividend, exercising captures the dividend while selling only recovers the shrinking time premium.

Frequently Asked Questions

When should a trader exercise a deep ITM option early instead of selling it?

Early exercise makes sense when remaining extrinsic value is less than the upcoming dividend for calls, or less than interest earned on the strike price for puts.

Why do premium sellers avoid writing deep ITM options?

The extrinsic value collected is minimal relative to capital at risk and margin required. A deep ITM short put might collect only $2 in extrinsic while requiring margin on $45,000 notional.

Related Terms

60/40 Tax Treatment

The favorable capital gains split applied to Section 1256 contracts where 60% of gains are taxed at the long-term rate and 40% at the short-term rate, regard...

Adjusted Option

An adjusted option is a listed contract whose terms — strike, multiplier, or deliverable — were modified by the OCC following a corporate action such as a st...

All-or-None Order

An all-or-none (AON) order is a time-in-force modifier requiring the entire order quantity to execute as a single transaction with no partial fills.

American-Style Option

An option contract that can be exercised by the holder at any time from purchase through expiration.

The information about Deep In-the-Money above is for educational purposes only and is not financial advice. Read our full investment disclaimer.

Apply Deep In-the-Money in practice

Use VolRadar tools to see Deep In-the-Money data live for any S&P 500 stock.

What to do next

See it in action

FreeCheck today’s Weather Score and ranked setups on the homepage.

See VRP, IV Rank, and signal strength for any S&P 500 stock.

Today’s pre-market analysis with regime interpretation and top picks.