Loading...

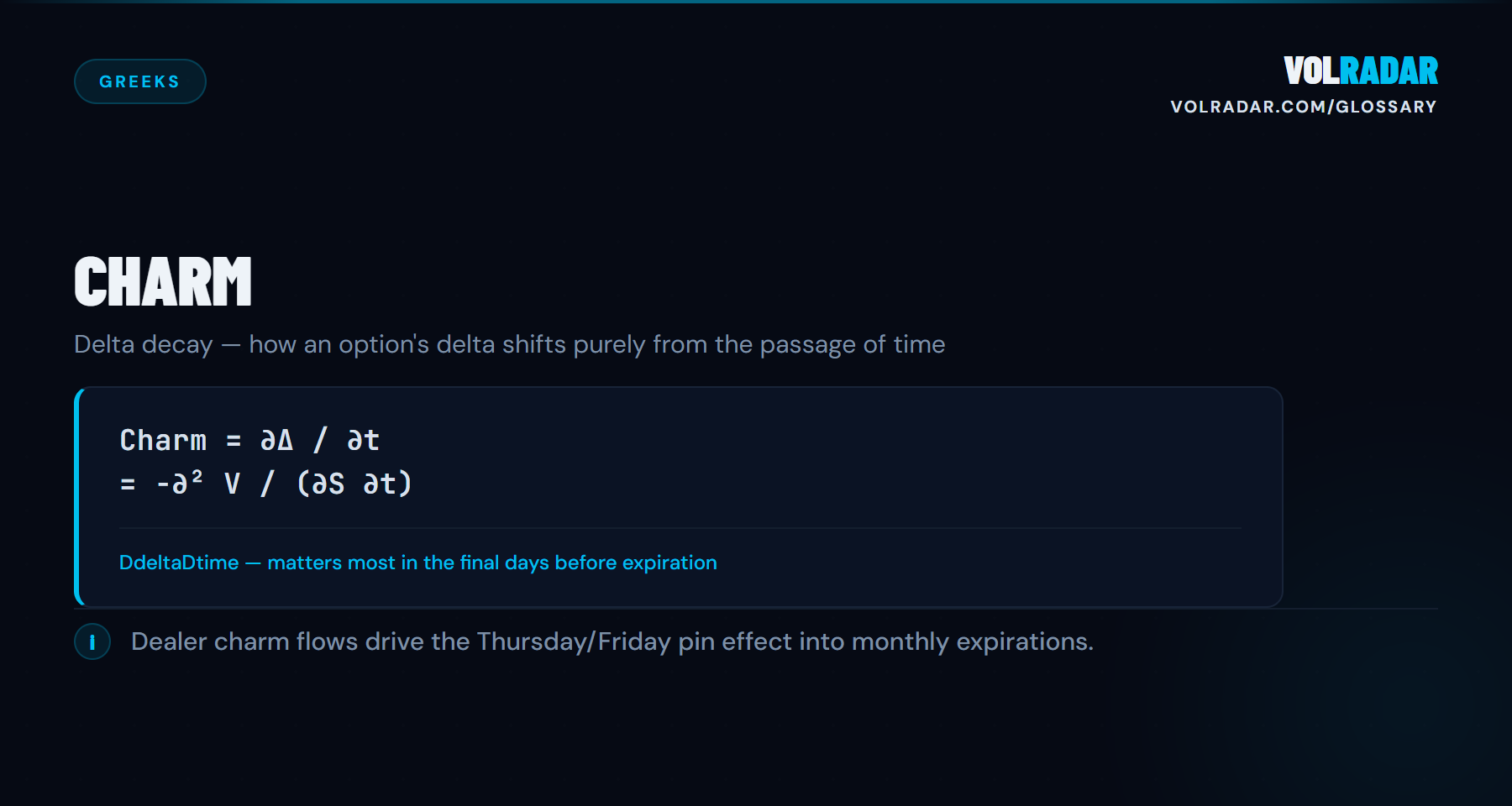

The rate at which delta changes as time passes (∂Δ/∂t), also called delta decay. A short OTM put's delta fades toward zero as expiration approaches — charm quantifies that drift. Sometimes grouped with higher-order Greeks.

⚡

Key takeawayCharm is your friend on short OTM positions — delta shrinks as time passes, reducing directional exposure automatically. It's the Greek that makes "time heals" literally true.

💡 Why It Matters

Charm is why short OTM positions feel safer as days pass even when the stock hasn't moved. Delta fades toward zero over time for OTM options — charm quantifies that drift. It's the Greek that makes the premium seller's 'time heals' intuition mathematically precise.

⚙ How It Works

Charm measures the rate of delta change per day (∂Δ/∂t). For a short OTM put, charm is positive — delta decreases (moves toward zero) as time passes. This means your directional exposure shrinks automatically without any price action. Charm accelerates as expiration approaches, especially for near-ATM options.

📋 Example

You sell a 45 DTE SPY put at 0.20 delta. Over 10 days with SPY flat, charm reduces your delta to approximately 0.16. Your directional risk dropped 20% without you doing anything — theta collected premium while charm reduced exposure.

⚠ Common Mistakes

Ignoring charm when rolling positions. If you roll from 20 DTE to 45 DTE at the same strike, your delta jumps back up because you've reversed the charm decay. Also: charm can work against you on ATM positions where delta moves toward 0.50 as expiration nears.

⚡ Charm in VolRadar

❓ FAQ

What is Charm?

The rate at which delta changes as time passes (∂Δ/∂t), also called delta decay. A short OTM put's delta fades toward zero as expiration approaches — charm quantifies that drift. Sometimes grouped with higher-order Greeks.

Why does Charm matter for premium sellers?

Charm is your friend on short OTM positions — delta shrinks as time passes, reducing directional exposure automatically. It's the Greek that makes "time heals" literally true.

How does Charm work?

Charm measures the rate of delta change per day (∂Δ/∂t). For a short OTM put, charm is positive — delta decreases (moves toward zero) as time passes. This means your directional exposure shrinks automatically without any price action. Charm accelerates as expiration approaches, especially for near-ATM options.

What are common mistakes with Charm?

Ignoring charm when rolling positions. If you roll from 20 DTE to 45 DTE at the same strike, your delta jumps back up because you've reversed the charm decay. Also: charm can work against you on ATM positions where delta moves toward 0.50 as expiration nears.

Related Terms

Color

The rate of change of gamma with respect to time.

Correlation Delta

Correlation delta (cega) measures an option's price sensitivity to changes in the correlation between underlying assets.

Delta

The rate of change in an option's price for a $1 move in the underlying stock.

Delta Hedging

Trading the underlying asset to offset an options position's directional exposure.

This is not financial advice. Read our full investment disclaimer.