Loading...

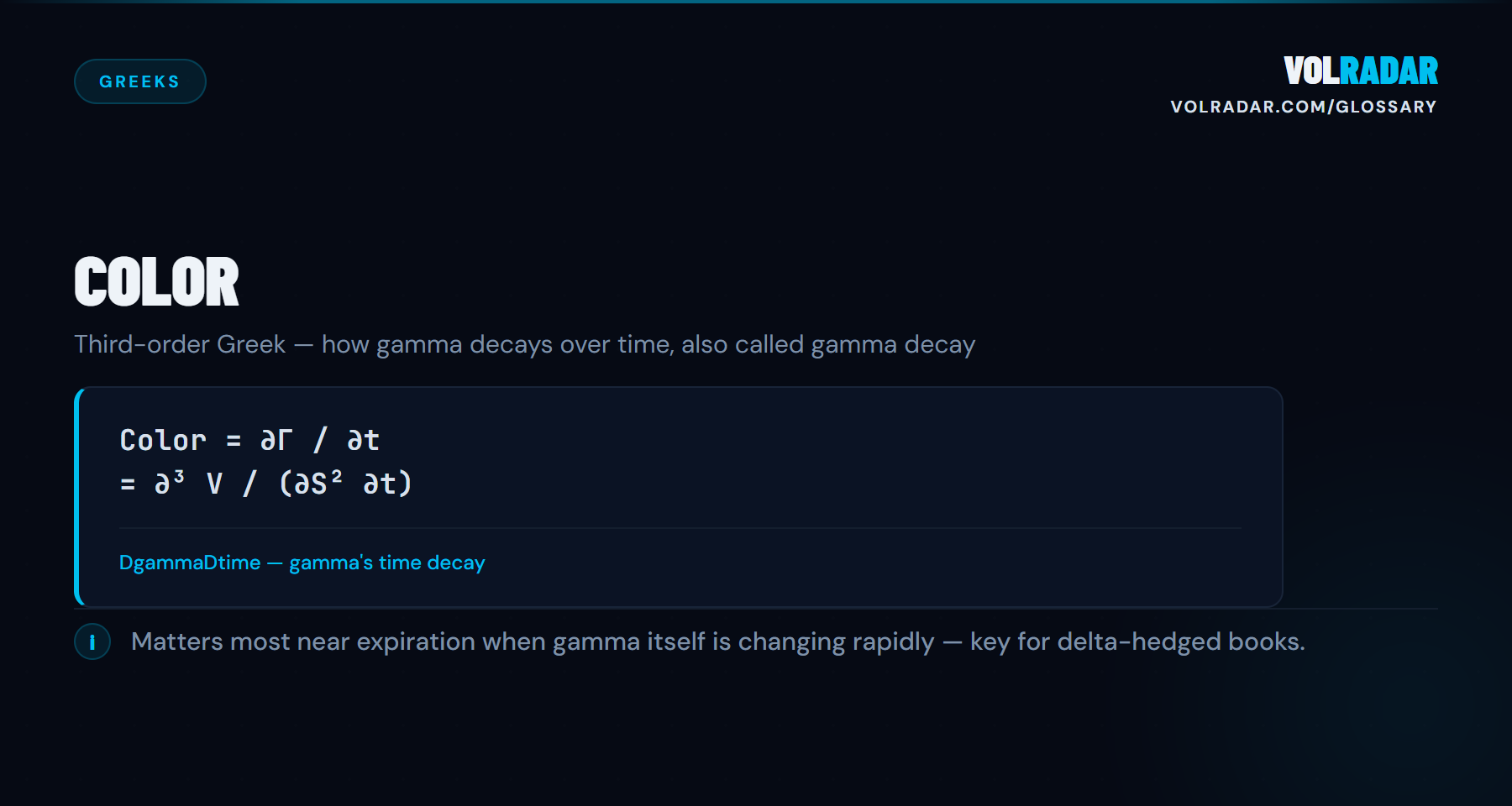

The rate of change of gamma with respect to time. Also called gamma decay.

⚡

Key takeawayColor explains why gamma risk accelerates near expiration even if the stock sits still.

💡 Why It Matters

Color explains why gamma risk escalates near expiration even when the stock doesn't move. As time passes, ATM gamma increases — color measures that acceleration. It's the reason premium sellers close positions by 21 DTE: gamma starts growing faster than theta can compensate.

⚙ How It Works

Color = ∂Γ/∂t (gamma decay or gamma bleed). For ATM options, color is positive — gamma increases as expiration approaches. For OTM options, color is typically negative — gamma decreases as the option becomes less likely to finish ITM. The net effect: ATM risk concentrates as time passes.

📋 Example

A short ATM SPY straddle at 30 DTE has gamma of 0.04. At 7 DTE with SPY unchanged, gamma has grown to 0.12 — three times higher. Color drove that increase. Each $1 SPY move now changes your delta by 12 shares instead of 4.

⚠ Common Mistakes

Holding short ATM positions into the last week because 'theta is highest.' Yes, theta accelerates — but so does gamma (via color). After 7 DTE, gamma often outpaces theta, making the position a net loser on risk-adjusted terms.

❓ FAQ

What is Color?

The rate of change of gamma with respect to time. Also called gamma decay.

Why does Color matter for premium sellers?

Color explains why gamma risk accelerates near expiration even if the stock sits still.

How does Color work?

Color = ∂Γ/∂t (gamma decay or gamma bleed). For ATM options, color is positive — gamma increases as expiration approaches. For OTM options, color is typically negative — gamma decreases as the option becomes less likely to finish ITM. The net effect: ATM risk concentrates as time passes.

What are common mistakes with Color?

Holding short ATM positions into the last week because 'theta is highest.' Yes, theta accelerates — but so does gamma (via color). After 7 DTE, gamma often outpaces theta, making the position a net loser on risk-adjusted terms.

Related Terms

Charm

The rate at which delta changes as time passes (∂Δ/∂t), also called delta decay.

Correlation Delta

Correlation delta (cega) measures an option's price sensitivity to changes in the correlation between underlying assets.

Delta

The rate of change in an option's price for a $1 move in the underlying stock.

Delta Hedging

Trading the underlying asset to offset an options position's directional exposure.

This is not financial advice. Read our full investment disclaimer.