Loading...

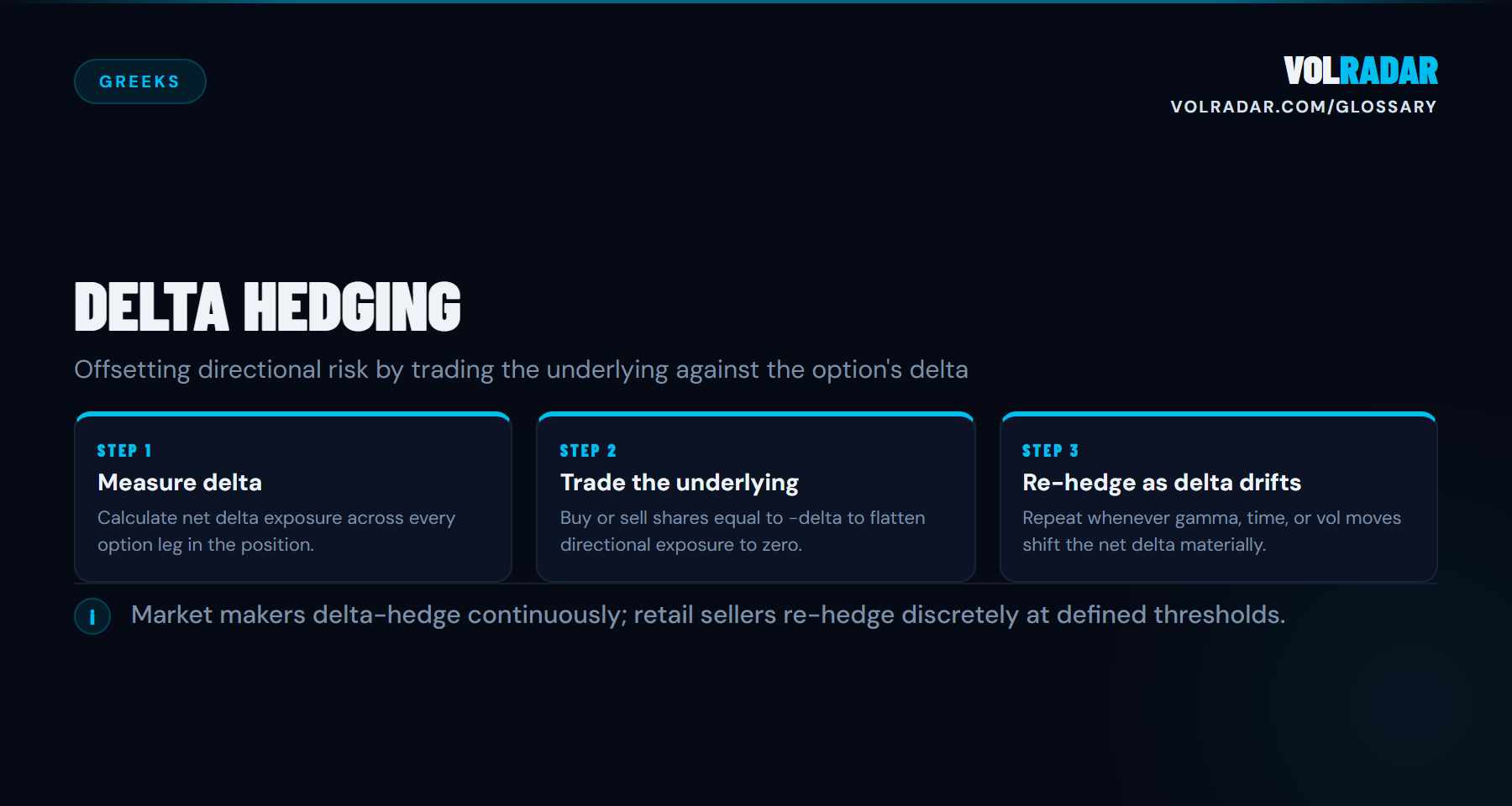

Trading the underlying asset to offset an options position's directional exposure. A market maker short 100 delta buys shares to neutralize. Retail sellers rarely delta-hedge — they manage via position sizing and rolling instead.

⚡

Key takeawayFull delta-neutral hedging is a market maker's game. Retail premium sellers manage delta risk through strike selection, sizing, and rolling — not continuous hedging.

💡 Why It Matters

Delta hedging is how market makers stay directionally neutral while providing liquidity. Retail sellers rarely hedge continuously, but understanding the concept explains why stocks pin near high-OI strikes at expiration and why dealer gamma exposure moves markets.

⚙ How It Works

A delta-neutral market maker offsets each option's delta by trading the underlying. Short 100 calls at 0.40 delta = short 4,000 shares of delta exposure, hedged by buying 4,000 shares. As the stock moves, delta changes (gamma), forcing the hedger to buy more on rallies and sell on drops — creating a stabilizing flow when gamma is positive.

📋 Example

A dealer sells 1,000 SPY 580 puts at 0.30 delta. Initial hedge: buy 30,000 shares of delta exposure (via futures). SPY drops $2, delta increases to 0.35. New hedge requirement: 35,000 shares. Dealer must sell 5,000 more — amplifying the down move if they're short gamma.

⚠ Common Mistakes

Retail traders attempting continuous delta hedging on small positions — commissions and slippage eat the edge. Also: confusing delta hedging with directional trading. Hedging removes directional risk; you're left harvesting theta and gamma, not betting on direction.

❓ FAQ

What is Delta Hedging?

Trading the underlying asset to offset an options position's directional exposure. A market maker short 100 delta buys shares to neutralize. Retail sellers rarely delta-hedge — they manage via position sizing and rolling instead.

Why does Delta Hedging matter for premium sellers?

Full delta-neutral hedging is a market maker's game. Retail premium sellers manage delta risk through strike selection, sizing, and rolling — not continuous hedging.

How does Delta Hedging work?

A delta-neutral market maker offsets each option's delta by trading the underlying. Short 100 calls at 0.40 delta = short 4,000 shares of delta exposure, hedged by buying 4,000 shares. As the stock moves, delta changes (gamma), forcing the hedger to buy more on rallies and sell on drops — creating a stabilizing flow when gamma is positive.

What are common mistakes with Delta Hedging?

Retail traders attempting continuous delta hedging on small positions — commissions and slippage eat the edge. Also: confusing delta hedging with directional trading. Hedging removes directional risk; you're left harvesting theta and gamma, not betting on direction.

Related Terms

Charm

The rate at which delta changes as time passes (∂Δ/∂t), also called delta decay.

Color

The rate of change of gamma with respect to time.

Correlation Delta

Correlation delta (cega) measures an option's price sensitivity to changes in the correlation between underlying assets.

Delta

The rate of change in an option's price for a $1 move in the underlying stock.

This is not financial advice. Read our full investment disclaimer.