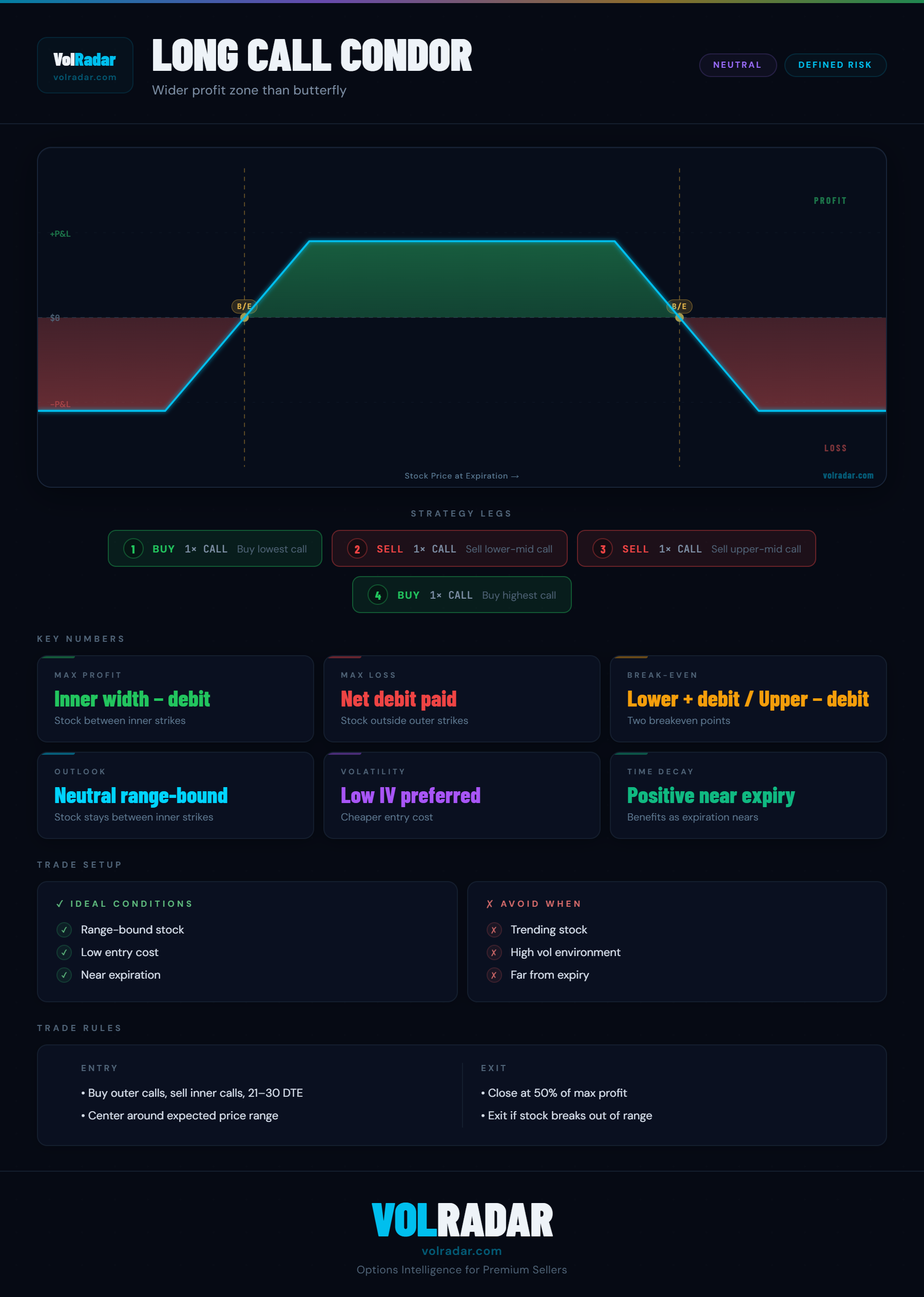

What is a long call condor?

A long call condor uses four strikes: buy 1 call at the lowest strike, sell 1 call at the second strike, sell 1 call at the third strike, buy 1 call at the highest strike. All at the same expiration. The position profits if the stock stays between the two short strikes at expiration. Unlike a butterfly (which has a single peak), the condor has a flat profit plateau between the inner strikes.

Long call condor vs iron condor

An iron condor uses both calls and puts (4 legs total with two credit spreads). A long call condor uses only calls (4 legs). The iron condor collects a net credit; the long call condor pays a net debit. The profit profile is similar (flat plateau between inner strikes) but the iron condor is more capital efficient since it collects premium upfront. Long call condors are less common in practice but useful when only call options are available or pricing is favorable.

When to use a long call condor

A long call condor is appropriate when IV is high (making the short options rich enough to fund the debit), the stock is expected to stay in a specific range, and you prefer to use only calls. The debit paid must be less than the inner spread width for a positive expected value. In most market conditions, the iron condor (credit structure) is preferred over the long call condor.

Risk and reward

Max profit equals the inner spread width minus the net debit, achieved when the stock is between the two short strikes at expiration. Max loss is the net debit paid. Breakevens are the lower short strike plus net debit and the upper short strike minus net debit. The ratio of max profit to max loss is the key metric — a long call condor needs to offer at least a 2:1 reward-to-risk to be worth the debit.