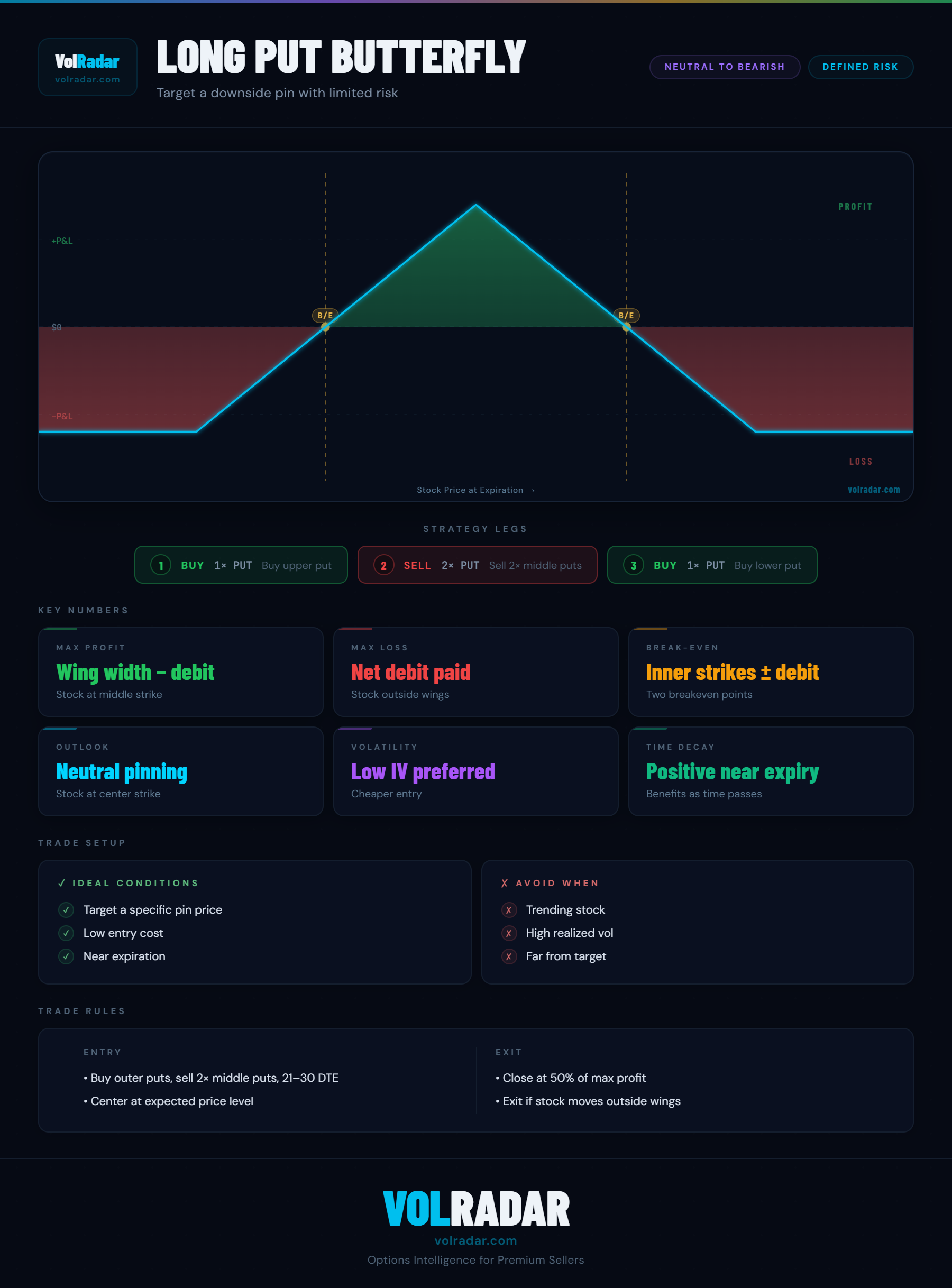

What is a long put butterfly?

A long put butterfly uses the same three-strike structure as a call butterfly but with put options: buy 1 put at the upper strike, sell 2 puts at the middle strike, buy 1 put at the lower strike. The net debit and risk profile are theoretically identical to a call butterfly with the same strikes, due to put-call parity. In practice, the choice between calls and puts depends on pricing and skew — whichever provides a cheaper debit is preferred.

Call butterfly vs put butterfly

In theory, long call and long put butterflies with the same strikes have identical payoffs. In practice, put options often have higher implied volatility than calls due to skew — meaning put butterflies may cost more (or less) than call butterflies depending on market conditions. Check both structures and choose the one with the smaller net debit. In bearish skew markets, call butterflies can be cheaper than put butterflies at the same strikes.

When to use a long put butterfly

Use a long put butterfly when you expect the stock to stay near a specific price and the put butterfly costs less than the equivalent call butterfly. It is also appropriate if you want to combine the butterfly with bearish outlook — a put butterfly centered below the current stock price acts as a defined-risk bearish pinning trade. The low debit keeps the risk minimal if the thesis is wrong.

Risk and reward

Max loss is the net debit paid. Max profit is the wing width minus the debit, achieved at the middle strike. Breakevens are the upper strike minus the debit and the lower strike plus the debit. As with call butterflies, the probability of maximum profit is low — the stock must pin near the middle strike. The low cost and high reward make it a speculative but defined-risk trade.