Loading...

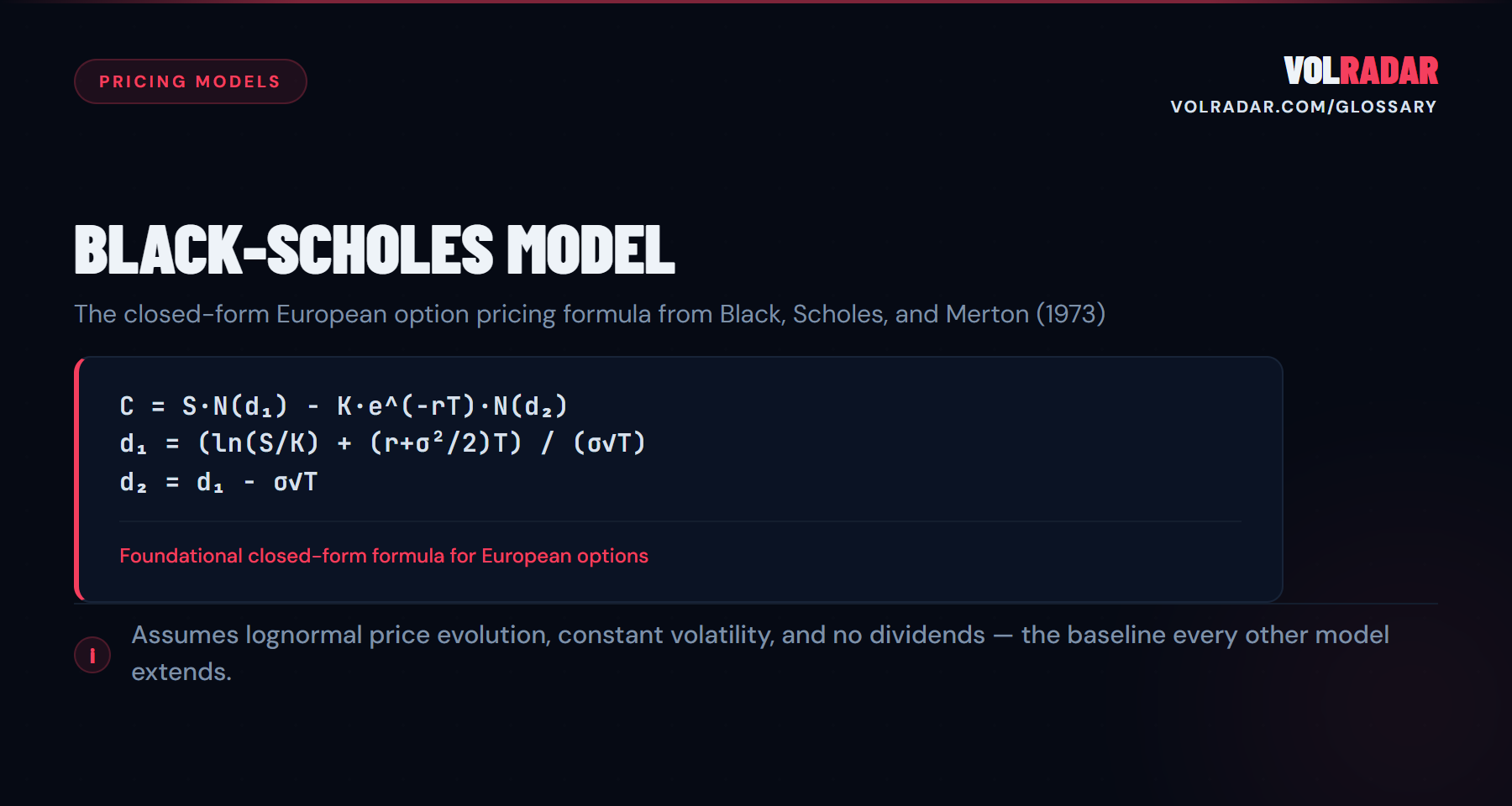

The foundational closed-form pricing model for European-style options, published in 1973. Derives option price from five inputs: spot price, strike, time to expiration, risk-free rate, and implied volatility. Assumes constant volatility and log-normal returns.

⚡

Key takeawayEvery broker price, every IV quote, every Greek you see traces back to Black-Scholes or a descendant. Understanding the five inputs matters more than memorizing the formula.

💡 Why It Matters

Every option price, every IV quote, and every Greek you see in your broker's platform traces back to Black-Scholes or a model descended from it. You don't need to memorize the formula, but understanding the five inputs and the model's assumptions tells you where it works and where it breaks.

⚙ How It Works

Five inputs → one output. Spot price (S), strike (K), time to expiration (T), risk-free rate (r), and implied volatility (σ) produce a theoretical option price. The model assumes constant volatility, log-normal returns, no dividends (in the basic form), and European exercise. Greeks are the partial derivatives of the formula.

📋 Example

S = $100, K = $100, T = 0.25 (3 months), r = 5%, σ = 20%. Black-Scholes produces a call price of approximately $4.62. Change σ to 30% (increase IV by 10 points) and the call jumps to $6.73. That $2.11 difference is pure vega — the model quantifies exactly how much IV matters.

⚠ Common Mistakes

Taking Black-Scholes prices as 'correct.' The model assumes constant volatility — which the volatility smile proves wrong. Real markets price OTM options higher than Black-Scholes predicts because of fat tails and jump risk. Black-Scholes is the starting framework, not the final answer.

❓ FAQ

What is Black-Scholes Model?

The foundational closed-form pricing model for European-style options, published in 1973. Derives option price from five inputs: spot price, strike, time to expiration, risk-free rate, and implied volatility. Assumes constant volatility and log-normal returns.

Why does Black-Scholes Model matter for premium sellers?

Every broker price, every IV quote, every Greek you see traces back to Black-Scholes or a descendant. Understanding the five inputs matters more than memorizing the formula.

How does Black-Scholes Model work?

Five inputs → one output. Spot price (S), strike (K), time to expiration (T), risk-free rate (r), and implied volatility (σ) produce a theoretical option price. The model assumes constant volatility, log-normal returns, no dividends (in the basic form), and European exercise. Greeks are the partial derivatives of the formula.

What are common mistakes with Black-Scholes Model?

Taking Black-Scholes prices as 'correct.' The model assumes constant volatility — which the volatility smile proves wrong. Real markets price OTM options higher than Black-Scholes predicts because of fat tails and jump risk. Black-Scholes is the starting framework, not the final answer.

Related Terms

Bachelier Model

The Bachelier model (normal model) assumes the underlying follows an arithmetic Brownian motion with normally distributed returns, rather than the lognormal ...

Barone-Adesi-Whaley Model

The Barone-Adesi-Whaley (BAW) model is a quadratic approximation for pricing American options that decomposes the American option price into its European val...

Binomial Option Pricing

A discrete-time pricing model that builds a recombining tree of possible price paths.

Bjerksund-Stensland Model

The Bjerksund-Stensland model provides a closed-form approximation for pricing American options by treating early exercise as a flat barrier problem.

This is not financial advice. Read our full investment disclaimer.