What is realized volatility?

Realized volatility is the actual, measured volatility of a stock over a historical window — typically 10, 20, or 60 trading days. It is computed from daily returns (log returns or close-to-close percentage changes) and annualised to match IV's scale. A 20% RV20d means the stock moved at a 20% annualised rate over the last 20 trading days. Unlike IV, which changes constantly with option prices, RV is a deterministic calculation that only updates when new price data arrives.

Close-to-close vs Yang-Zhang

The simplest RV calculation uses only daily closing prices — close-to-close volatility. It is easy but ignores intraday movement. The Yang-Zhang estimator uses open, high, low, and close (OHLC) data from each day, capturing both overnight gaps and intraday range. Yang-Zhang is 7–8× more statistically efficient per data point than close-to-close, making it the preferred method for accurate RV measurement. VolRadar displays Yang-Zhang RV10/20/60 on ticker pages for comparison.

Why it matters for premium sellers

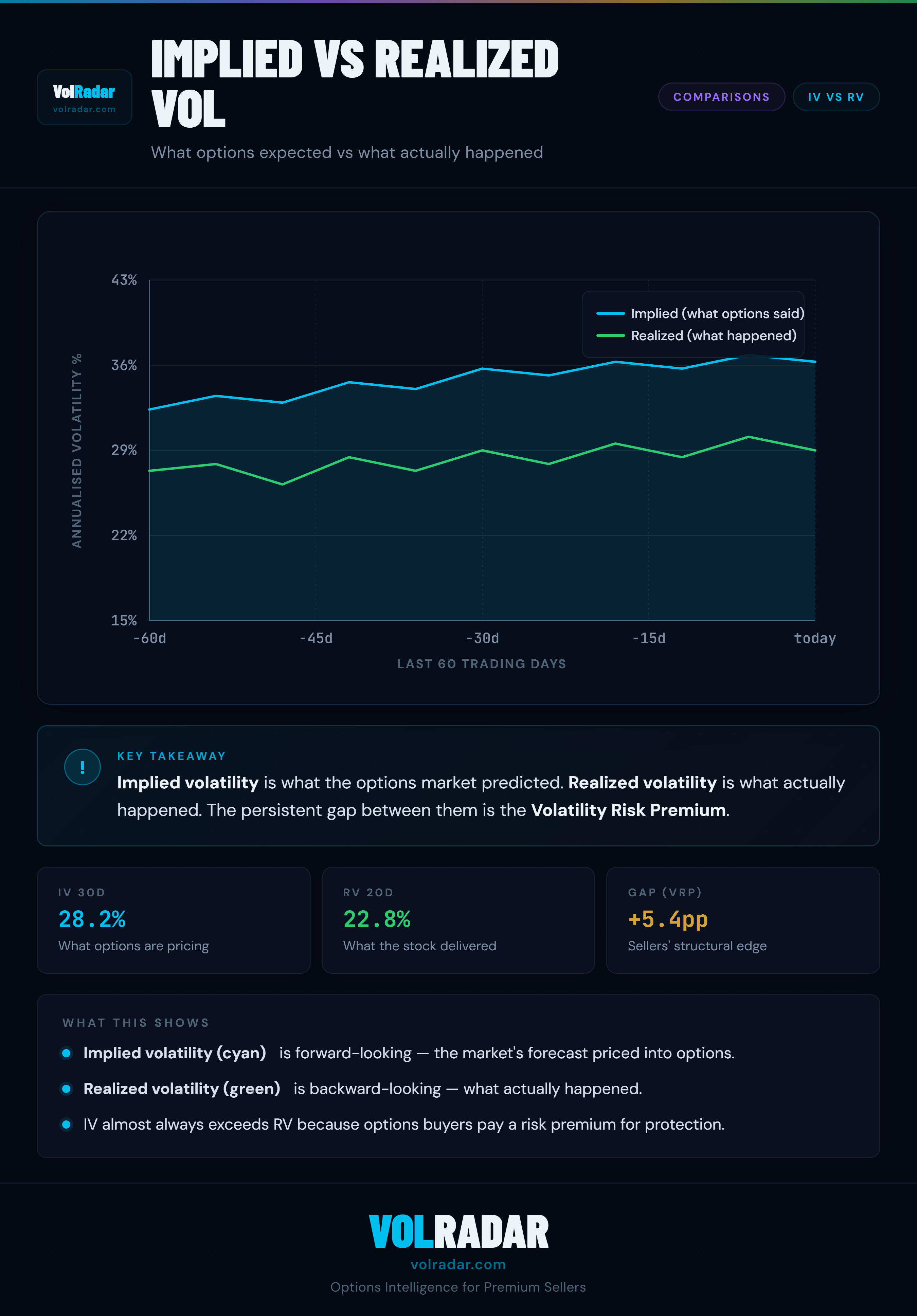

Realized volatility is the benchmark against which implied volatility is judged. If RV consistently comes in below IV, options were overpriced and premium sellers made money. If RV exceeds IV, options were underpriced and sellers lost. The structural edge in premium selling exists because IV averages 3–5 percentage points above RV for large-cap stocks. That gap — the Volatility Risk Premium — is what sellers harvest.

Measurement windows

VolRadar computes RV at 10d, 20d, and 60d windows. RV10d reacts fastest to recent moves but is noisy. RV60d is smoother but lags. RV20d is the default for VRP and RV Ratio calculations because it balances responsiveness and stability. When trading around specific events (earnings, catalysts), RV10d is more useful; for regime assessment, RV60d gives a cleaner signal.