What is implied volatility?

Implied volatility is the volatility figure implied by an option's market price. Option pricing models (Black-Scholes and its variants) take inputs like stock price, strike, time to expiration, and interest rate — the one number left to solve for is volatility. That solved volatility is "implied". IV is quoted as an annualised percentage: 30% IV on a $100 stock means the market is pricing in roughly a $30 one-standard-deviation range over a year.

What moves implied volatility

IV rises when demand for options increases — typically before earnings, Fed decisions, macro data releases, or broader market stress. IV falls when uncertainty resolves — most visibly after earnings announcements, where IV can collapse 30–60% in hours (the "IV crush"). Supply and demand for downside protection also drive IV: during sharp selloffs, IV spikes as traders buy puts faster than market makers can hedge.

Why premium sellers care

Selling premium is a bet that realised volatility will be lower than implied volatility. When IV is elevated, options are expensive — meaning the premium you collect is large relative to the actual movement you expect. When IV is low, premiums are thin and do not compensate you fairly for the risk. The best premium selling conditions combine elevated IV (high IV Rank) with a history of realised vol undershooting implied (positive VRP).

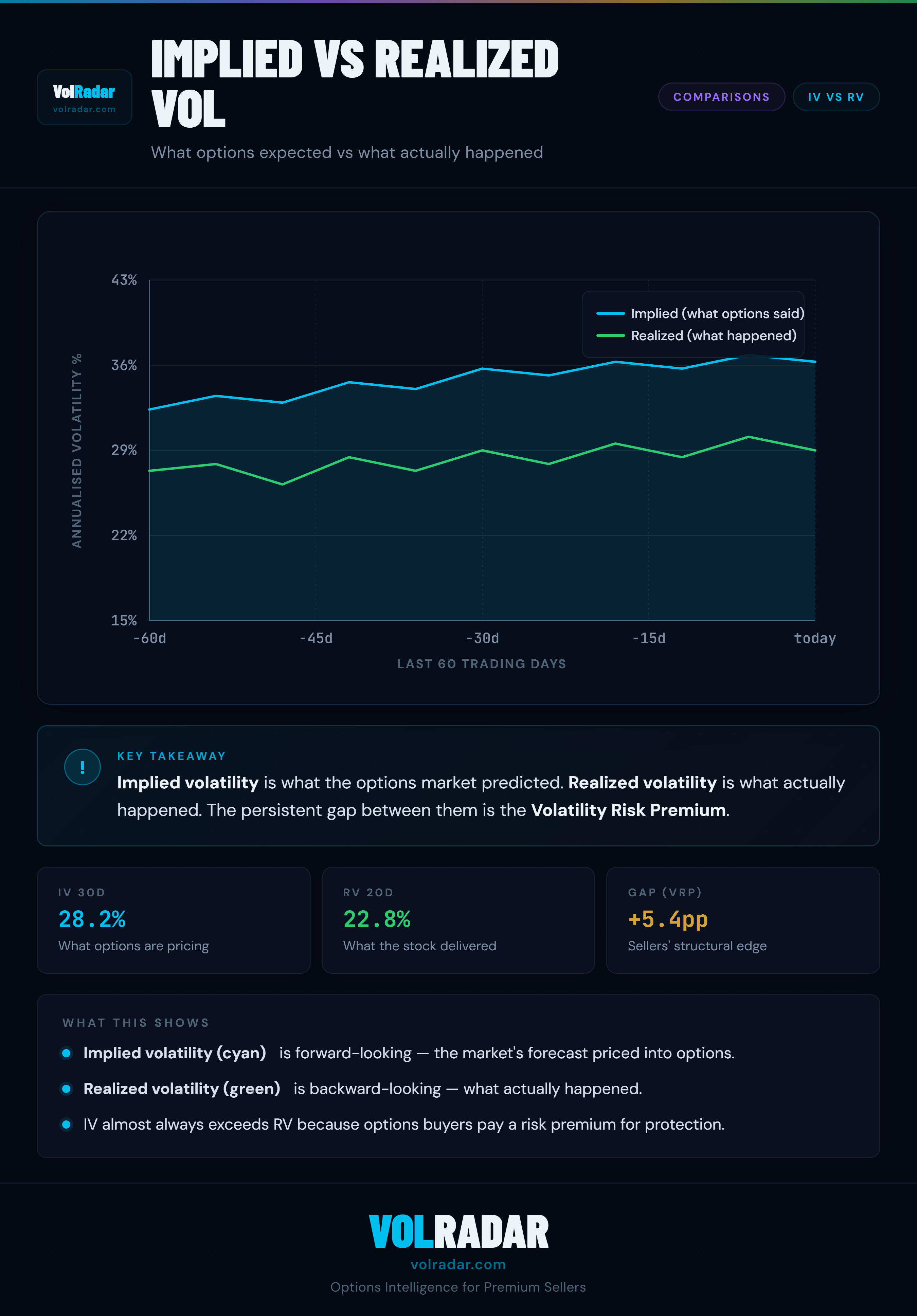

IV vs Historical Volatility

Implied volatility is forward-looking; historical (realised) volatility is backward-looking. IV tells you what the market expects going forward, HV tells you what actually happened. The persistent gap between IV and HV is the Volatility Risk Premium — the structural edge that makes premium selling profitable over time. VolRadar displays both side by side on every ticker page so you can see the gap instantly.