What is an inverse iron condor?

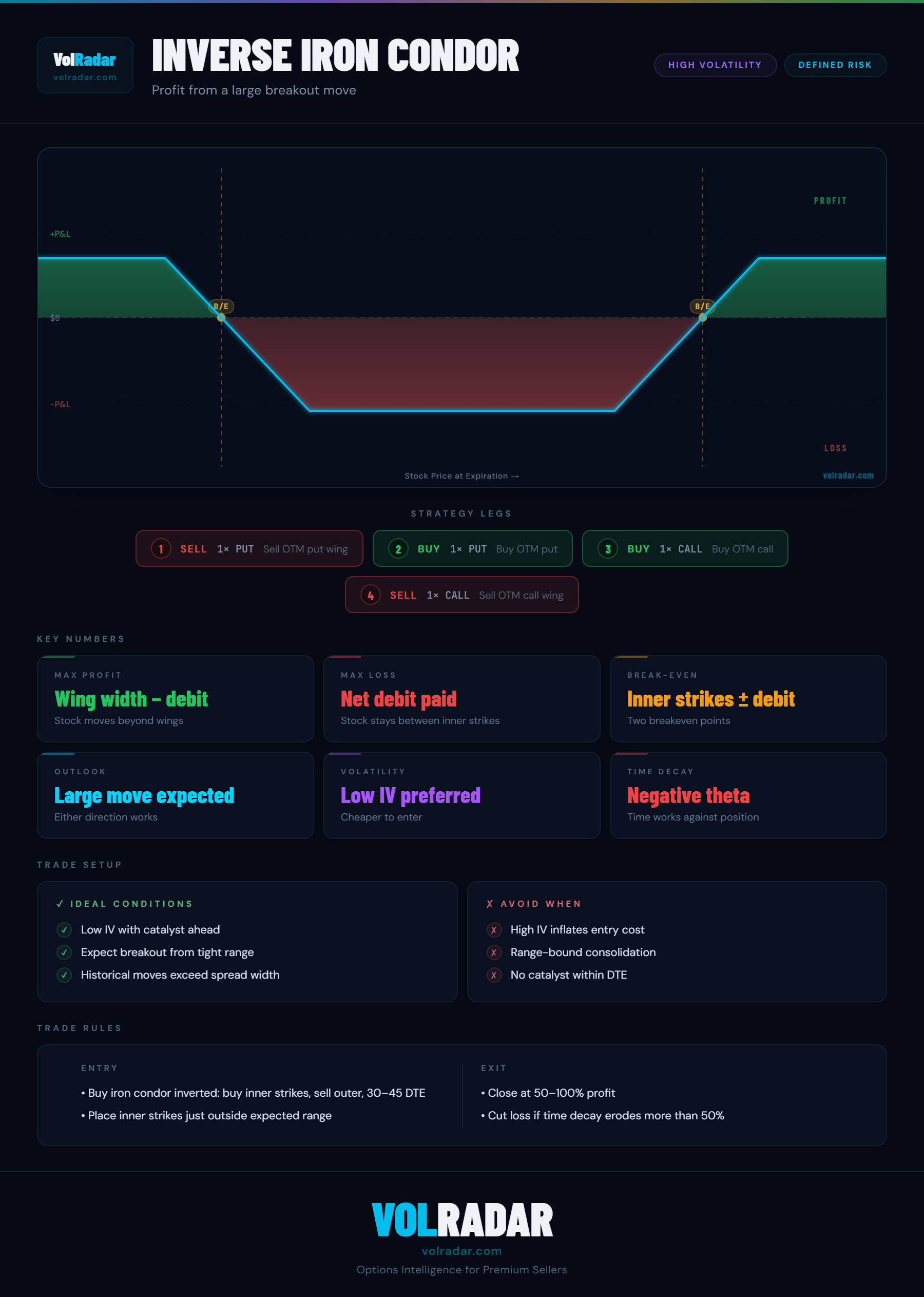

An inverse iron condor reverses the standard iron condor: buy 1 OTM call and 1 OTM put (strangle), then sell 1 further OTM call and 1 further OTM put (wings). You pay a net debit. The position profits when the stock moves significantly in either direction — the OTM long strangle allows a wider profit range than the ATM inverse iron butterfly. The short wings cap the maximum profit and reduce the net cost.

Inverse iron condor vs inverse iron butterfly

The inverse butterfly uses ATM options (highest premium, widest immediate sensitivity). The inverse condor uses OTM options (lower premium, requires a larger initial move before profiting but covers a wider range). The inverse condor is appropriate when you expect a large but uncertain direction move and want the profit zone to extend further from the current price.

When to use an inverse iron condor

Use when you expect a large volatility event and want the widest possible profit range within a defined-risk structure. The OTM long strikes mean the stock must move more than with an inverse butterfly before becoming profitable — but the profit zone extends further out. Best used when the expected move is large and uncertain in direction: earnings on high-IV stocks, macro data releases, FDA decisions.

Risk and reward

Max loss is the net debit paid, occurring when the stock stays between the long strikes at expiration. Max profit is the inner spread width (between long and short options) minus the debit. Breakevens are the long call strike plus debit and long put strike minus debit. The position benefits from rising IV (long vega) — entering before an expected IV spike improves the risk-to-reward significantly.