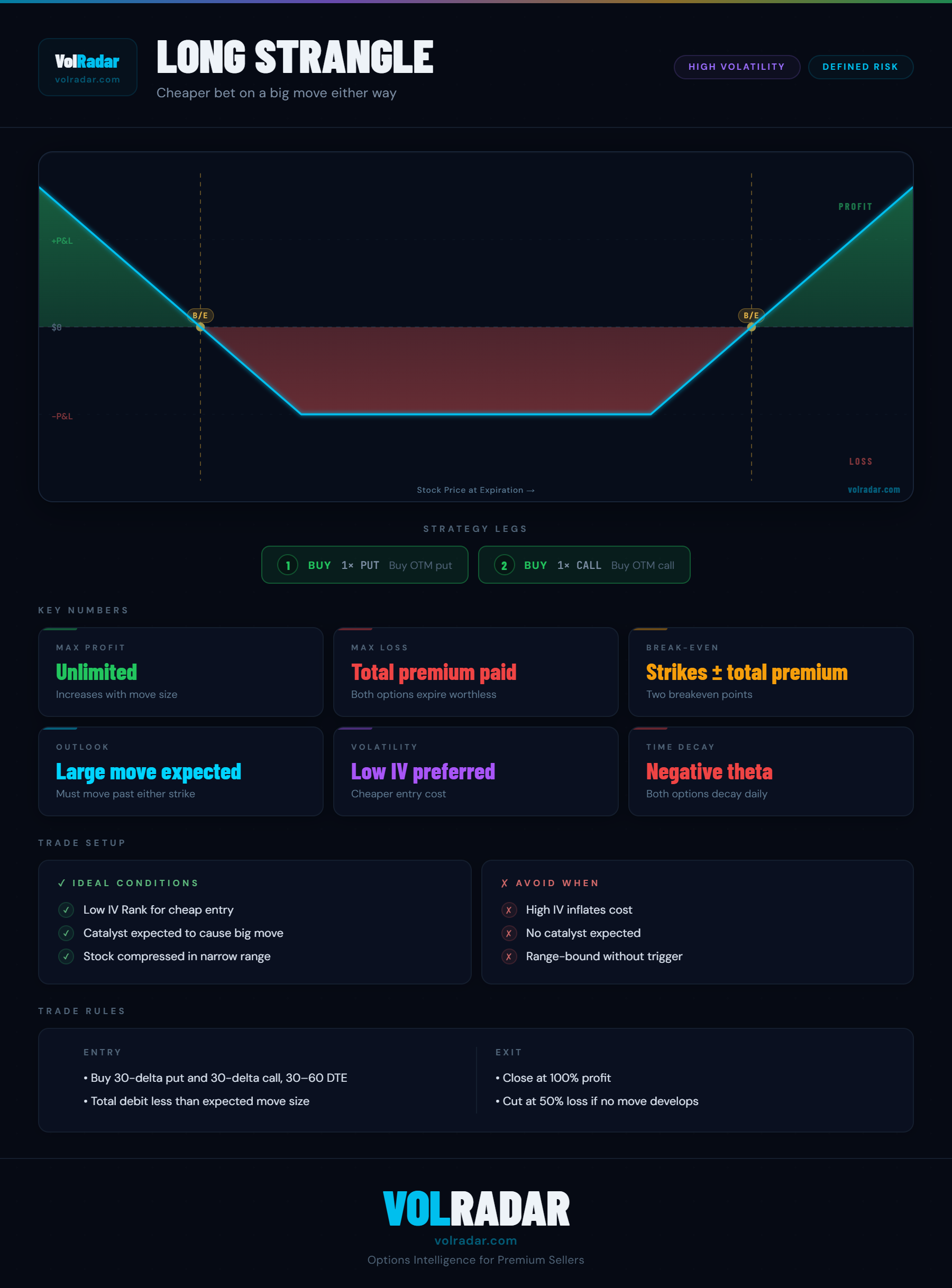

What is a long strangle?

A long strangle buys 1 OTM call above the current stock price and 1 OTM put below the current stock price at the same expiration. Both options are out-of-the-money at entry, making the total cost lower than a long straddle. The position profits if the stock moves significantly in either direction beyond the breakeven levels. Max loss is the total premium paid.

Long strangle vs long straddle

A long straddle uses ATM options — maximum sensitivity, highest cost, breakeven closest to current price. A long strangle uses OTM options — lower cost, but the stock must move further before the position profits. As a rule of thumb: use a straddle when you expect a big move and want maximum sensitivity; use a strangle when you want to reduce the premium paid and are willing to require a larger move to reach profitability.

Strike selection for strangles

Choose call and put strikes based on the expected move range. The 16-delta strikes (1 standard deviation OTM) are a common starting point. Wider strikes cost less but require a larger move. For earnings plays, setting the strangle strikes just outside the "earnings implied move" range (where the straddle is priced) creates an inexpensive play if the stock moves more than the market expects.

Managing a long strangle

The same time decay risk applies as with straddles: theta erodes the value of both options daily. Close at 100–200% profit on the overall position. If the stock moves toward one side, close the profitable option and decide whether to hold the other as a lottery ticket or close the full position. Set a time-based stop (close at 50% DTE if position is unprofitable) to limit ongoing theta losses.