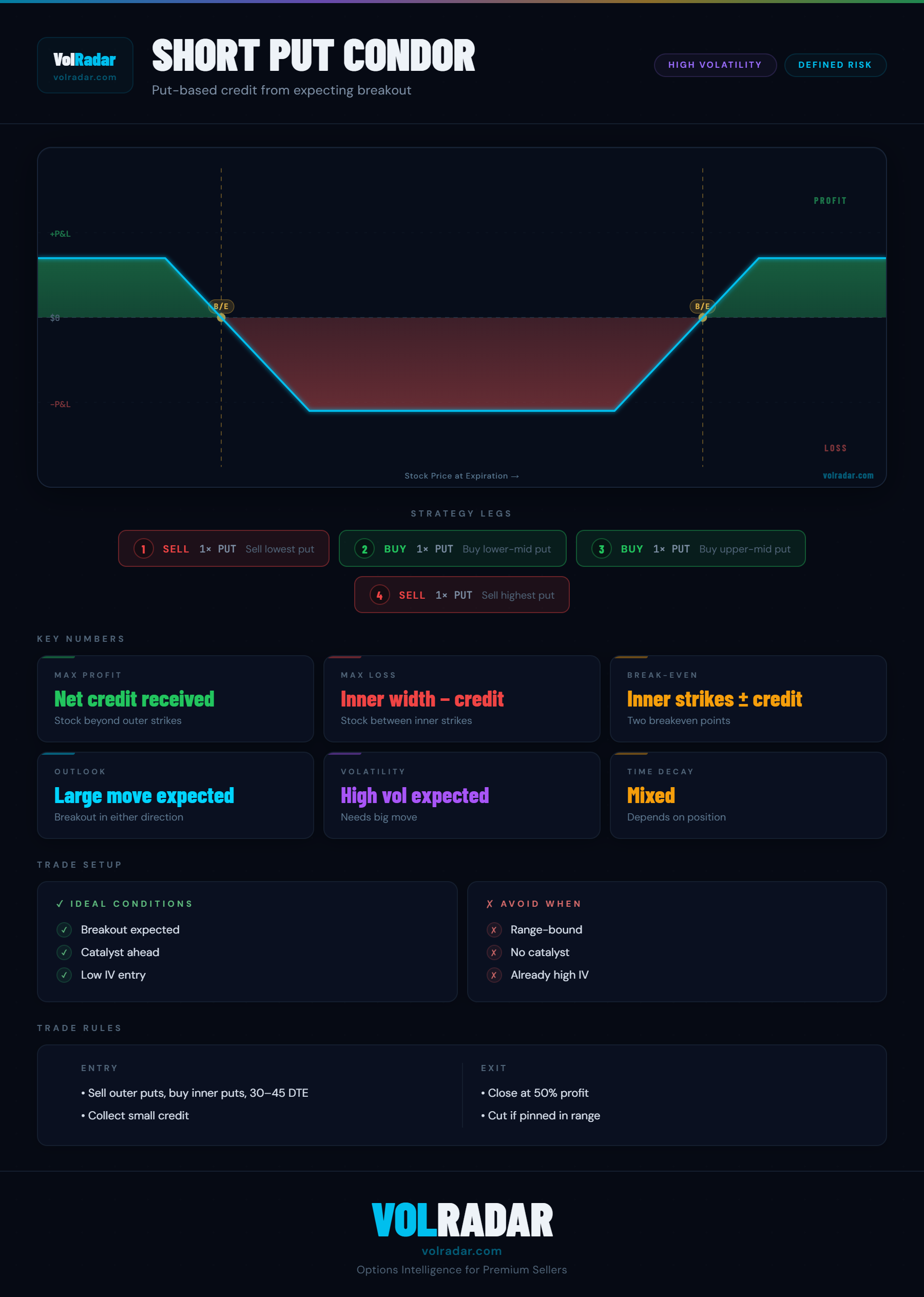

What is a short put condor?

A short put condor uses four put strikes: sell the outermost puts (highest and lowest) and buy the inner two puts. The net credit received is the maximum profit if the stock moves significantly. Like the short call condor, it profits on large moves and loses when the stock stays near the inner strikes. Due to put-call parity, the short put and short call condor at the same strikes have identical theoretical payoffs.

Choosing between short call and short put condors

Due to put-call parity, the payoffs are identical at the same strikes. The choice depends on which offers better pricing. In high put skew markets, the outer short puts collect more premium — potentially making a short put condor more attractive. Compare the net credit offered by both structures before deciding. Liquidity at each strike also matters — choose the structure with tighter bid-ask spreads.

Risk and reward

Max profit is the net credit collected, realized if the stock moves outside either outer wing. Max loss is the inner spread width minus the credit. The position is essentially two bull put spreads (or a call condor equivalent) inverted. Manage by closing when the move occurs and the target profit is reached — do not hold to expiration hoping for more profit as gamma risk increases.

Practical considerations

Short condors are less common than long condors or iron condors in retail trading. They require specific market views (large moves) and careful strike selection. They are most useful in binary event situations — earnings, FDA announcements — where a defined-risk structure is preferable to an open-ended long straddle or strangle. Always model the P&L before entering to confirm the credit justifies the risk.